The single column cash book resembles a T-shaped cash account in almost all respects. The pages of this book are vertically divided into two equal parts.

The receipts are entered on the left (debit) side. Payments are entered on the right (credit) side.

A single column cash book has only one money column on the debit and credit sides to record cash transactions.

This is the reason why it is called a single column cash book (or a simple cash book).

A single column cash book records only cash receipts and payments.

This form of a cash book has only one amount column on each of the debit and credit sides of the cash book.

All the cash receipts are entered on the debit side, and cash payments are entered on the credit side.

In essence, a single column cash book is nothing but a cash account. A cash account cannot show a credit balance on the principle that you cannot pay what you do not have.

This means that a cash account always shows a debit balance or nil balance.

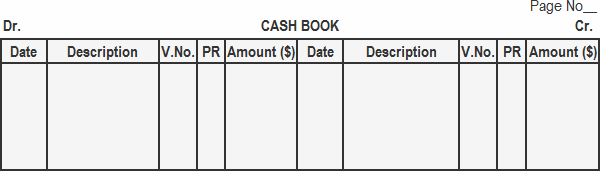

The standard format of a single column cash book is shown below.

The format above consists of five columns on both sides of the cash book. The purpose/function of each column is briefly described in this section.

The year, month, and day of the receipts and payments of cash are written in the date column on the debit and credit sides of the cash book.

Don't repeat the year and month for additional entries until a new month starts (or a new page is added).

The description column starts with the words "balance brought down" or simply "balance."

This column shows the cash balance at the start of the current period. After recording the opening balance in the description column, the cash transactions of the current period are recorded.

When cash is received on an account, the name of that account is written on the debit side. When cash is paid on an account, the name of the account is written on the credit side in the description column.

For every entry recorded in the cash book, there must be a proper voucher.

When money is received, an original receipt is given to the payer and the payee retains a copy.

This receipt is called a debit voucher because it supports the entries on the debit side of the cash book.

When a payment is made, an original receipt is obtained from the payee. This receipt is called a credit voucher because it supports entries on the credit side of the cash book.

The debit voucher's serial number is recorded on the debit side, and the serial number of the credit voucher is recorded on the credit side in the cash book's voucher number (V. No.) column.

When entries from the cash book are posted to ledger accounts, the relevant account number is written in this column.

The amount column is used to enter the amount received or paid as a result of a cash transaction.

At the end of the day, or at the end of the accounting period, the amount columns on both sides are totaled.

The cash column's total on the debit side will always exceed the total of the credit side. This is because we cannot pay more cash than we have received.

The difference represents the actual cash in hand, which should agree with the amount of cash in the cash box.

To make the two sides of the single column cash book equal, the difference is written on the credit side as "balance carried down" or simply "balance."

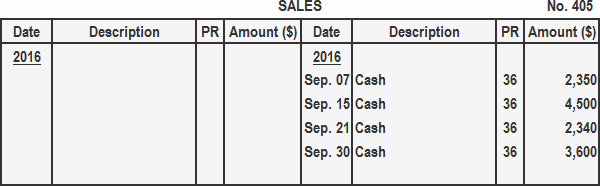

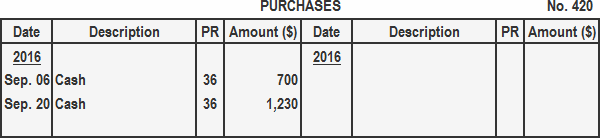

The following points should be kept in mind when posting the single column cash book to the relevant accounts in the ledger.

First, the opening and closing balances of the cash book are not posted.

Second, the items on the debit side of the cash book are posted to the credit sides of the accounts in the ledger, and the respective account numbers are entered in the posting reference column of the cash book.

Finally, the items on the credit side of the cash book are posted on the debit sides of the accounts in the ledger, and the respective account numbers are entered in the posting reference column of the cash book.

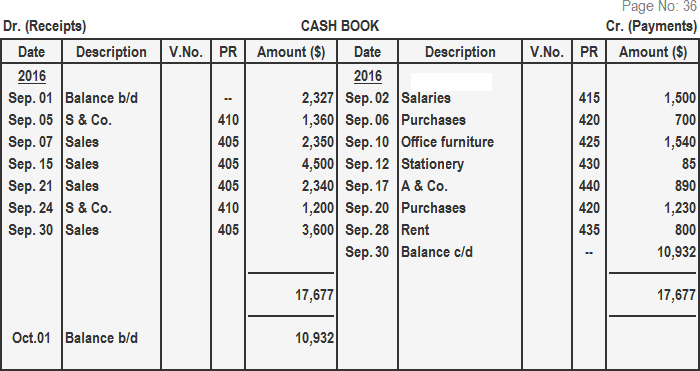

Record the transactions shown below in a single column cash book and post to the ledger.

For the year 2016, the transactions are as follows:

The single-column cash book resembles a t-shaped cash account in almost all respects. A single column cash book has only one money column on the debit and credit sides to record cash transactions. This is the reason why it is called a single column cash book (or a simple cash book).

The pages of this book are vertically divided into two equal parts. The receipts are entered on the left (debit) side. Payments are entered on the right (credit) side.

A double-column cash book includes separate columns for recording receipts and payments, while a single-column cash book combines both types of transactions into one column. As such, the single-column cash book provides less detailed information than the double-column cash book.

To prepare a single-column cashbook, simply record all cash receipts and payments made by the business in a single column, with the net amount of cash on hand represented as a balancing figure.

The purpose of a single-column cash book is to provide a quick and easy way to track all cash receipts and payments made by a business during a given period of time. It is also useful in determining the net amount of cash on hand at the end of the period.

About the Author

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.

Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own.

Content sponsored by 11 Financial LLC. 11 Financial is a registered investment adviser located in Lufkin, Texas. 11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. 11 Financial’s website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links.

For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing. A copy of 11 Financial’s current written disclosure statement discussing 11 Financial’s business operations, services, and fees is available at the SEC’s investment adviser public information website – www.adviserinfo.sec.gov or from 11 Financial upon written request.

11 Financial does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to 11 Financial’s website or incorporated herein, and takes no responsibility therefor. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

© 2024 Finance Strategists. All rights reserved.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.